Service Design x Behavioural Economics: Midterm Mortgage Retention Project (2022-2023)

(This was a long-ish project. If you're looking for a quick summary, check out the TL;DR version. If you're a service design or behavioural economics enthusiast—or just nerdy enough like me to dive into the research methods—I invite you to read the whole thing!)

My Role: Co-lead Service Designer

TL;DR:

This end-to-end service design project aimed to understand why mortgage clients switch providers mid-term (before mortgage maturity) even when facing penalty fees. The goal was to identify opportunity areas and develop potential solution areas to improve retention effort.

We conducted a range of primary and secondary research activities, including client interviews, call listening & call centre agent job shadowing, secondary research, co-creation sessions & ideation workshops, intervention testing, and surveys)

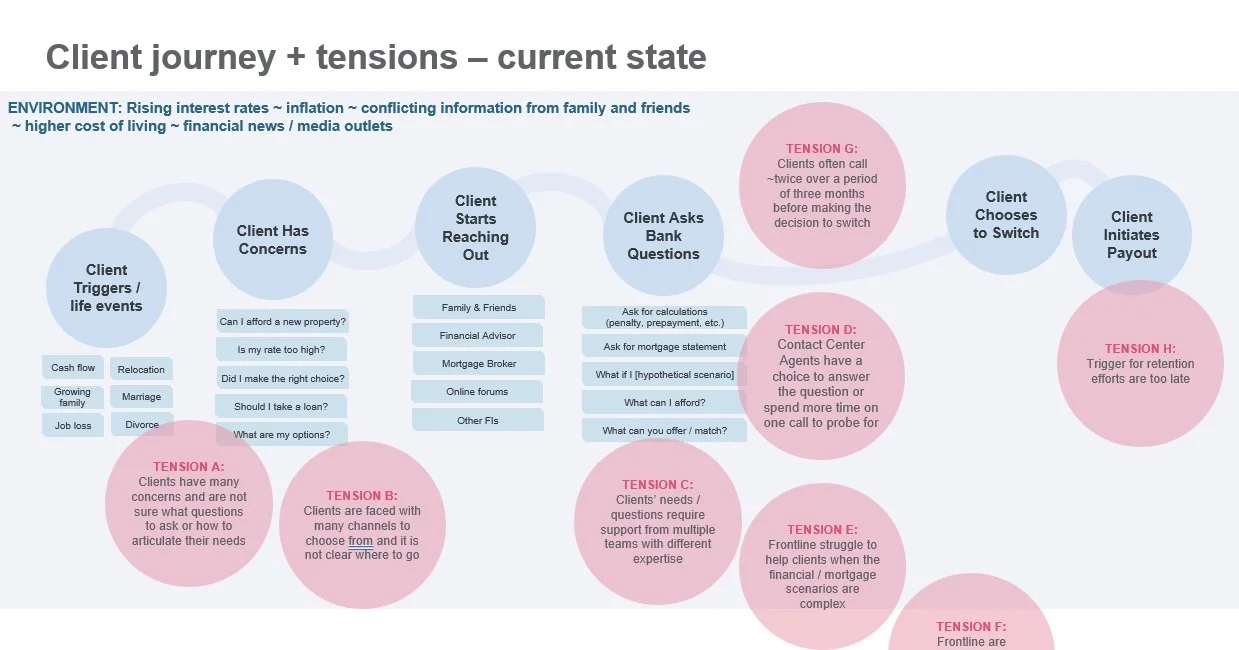

Using these methods, we mapped the current-state client journey and identified key pain points and trigger points that influence clients’ decisions.

Based on the research findings, we identified a key problem area to target: Clients do not turn to the bank early in their decision-making process. By the time they reach out, they’ve often already made up their minds to switch, leaving little room for the bank to intervene effectively.

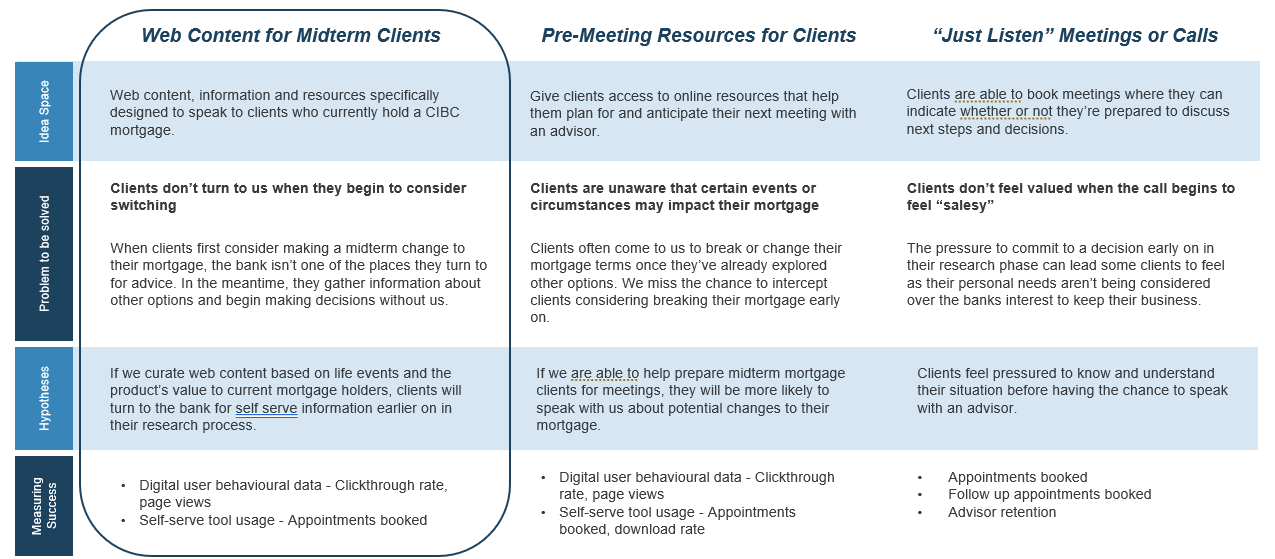

After an ideation and prioritization workshop with stakeholders, we focused on designing a webpage for existing mortgage clients who are beginning their research process.

Through current-state website analysis, I identified an opportunity to redesign the Contact Us CTA section using insights from Behavioural Economics. This intervention aimed to address the "last mile" problem—those moments where an end-user directly interacts with a product or service. "How might we redesign the Contact Us CTA section to encourage clients to engage with the bank earlier in their research process—before it’s too late?"

I designed and tested two nudging interventions, one of which was implemented on the newly developed Manage My Mortgage webpage on the bank’s website.

Business Objective

Identify pain points and trigger points along the current mortgage client’s journey, understand the drivers of mortgage clients’ decisions to switch or stay with their provider, and identify tactics that help clients make optimal mid-term decisions, in order to increase the rate of mid-term retention and lower mid-term attrition.

Research Methods

A mixed-methods approach, incorporating both primary and secondary research.

Behavioural & Psychological Barriers

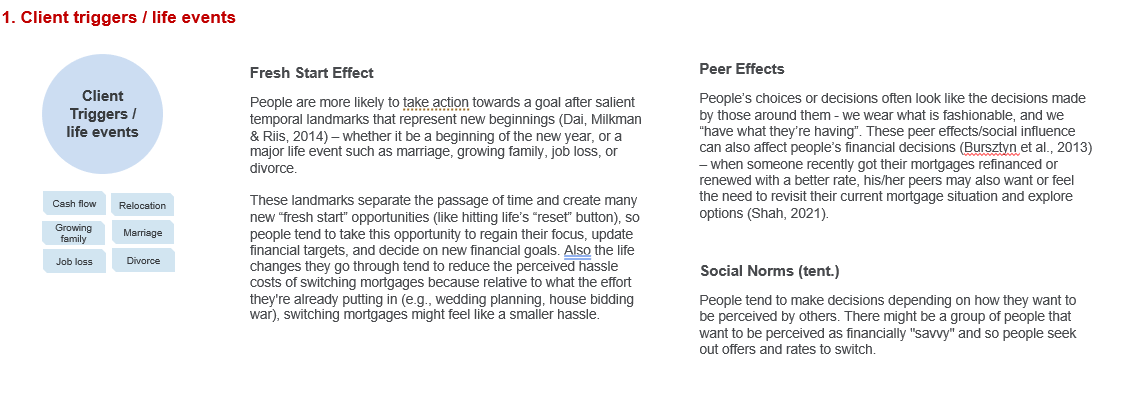

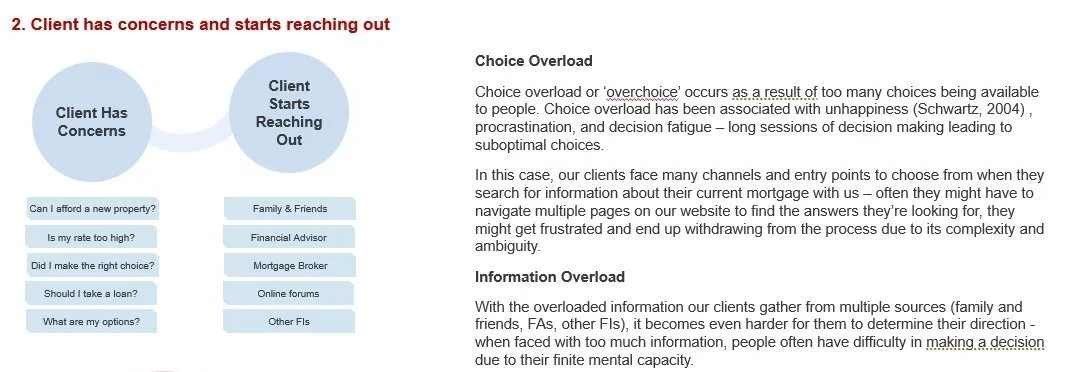

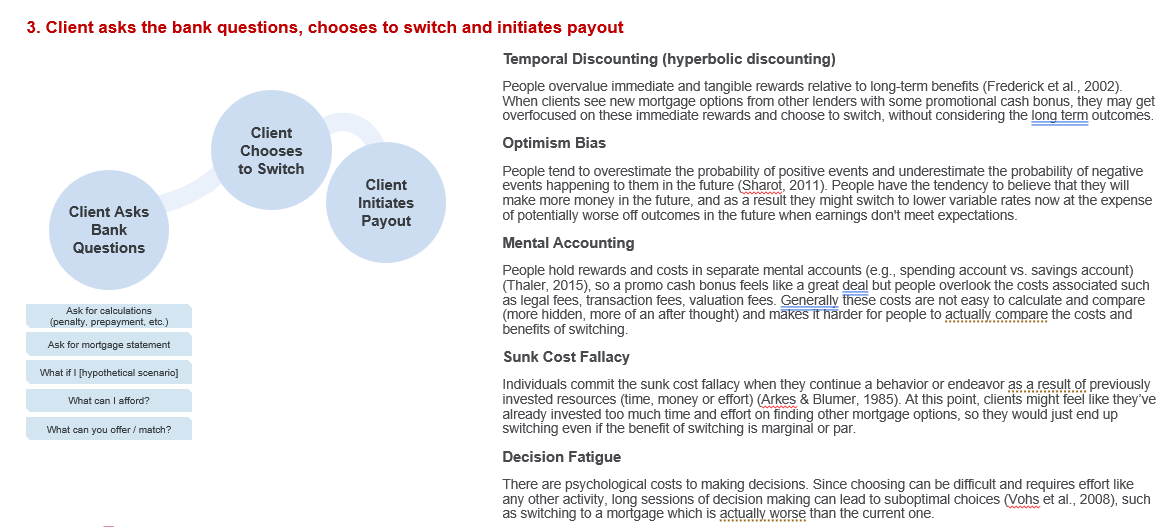

As we mapped out the current state journey, I provided Behavioural Economics principles to help us better understand what are some underlying psychology behind the clients’ behaviour in the current state journey.

Basically, what could possibly be going on in their head at each decision point.

Key Problem Identified

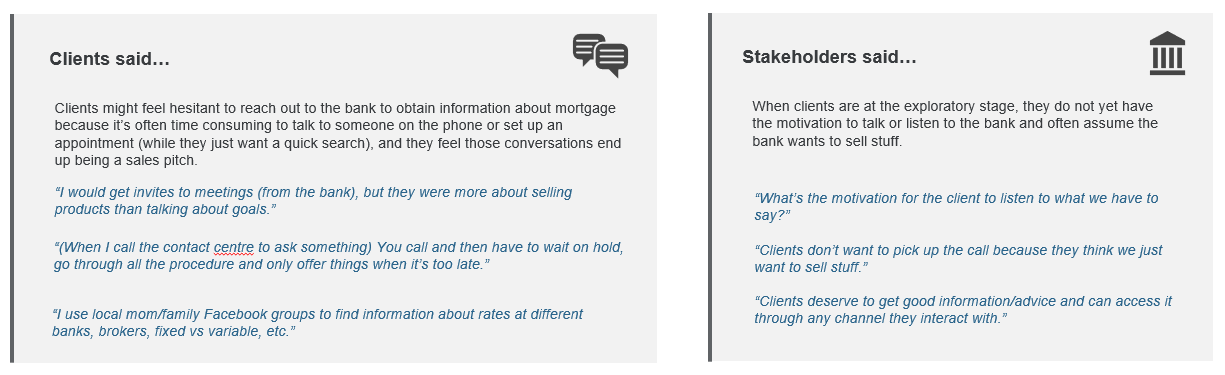

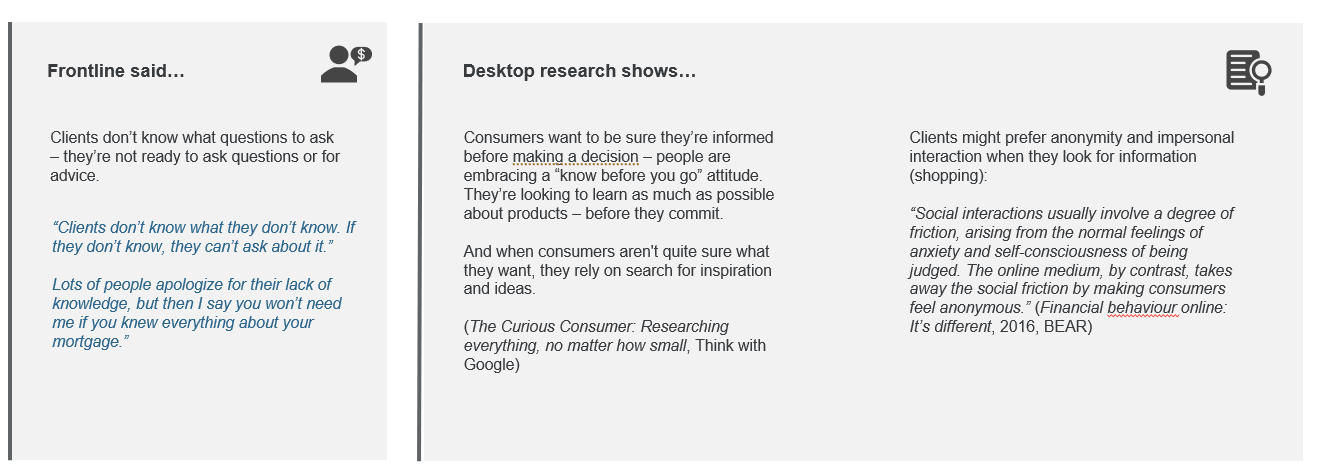

After the mixed methods research activities and internal stakeholder workshops, the key problem area we aimed to target in this project was when clients first consider making a change to their mortgage, the bank isn’t one of the places clients turn to.

They start their exploratory research to look for information but at this stage they are just looking to do a quick scan of the market or gather information with no or little intention of making any decision.

At this point in the client’s journey, talking to someone at the bank might feel too early in the process or they may not be ready to commit the time and energy to a conversation. In the meantime, clients are learning about other options and making decisions without us.

After an ideation and prioritization workshop with stakeholders, we focused on designing a webpage for existing mortgage clients who are beginning their research process.

BE Project: Solving the ‘Last Mile’ Problem – Using Behavioural Insights to Encourage Clients to Contact the Bank

After conducting a landscape analysis of the bank’s existing web environment, I identified an opportunity to redesign the Contact Us CTA section using behavioural insights. This redesign could play a critical role in driving behaviour change by addressing challenges at the "last mile" problem—those moments where an end-user directly interacts with a product or service.

"How might we redesign the Contact Us CTA section to encourage clients to engage with the bank earlier in their research process—before it’s too late?"

Target Audience:

Existing mortgage clients who prefer to conduct their own research before speaking with the bank. These clients typically:

Only reach out when they feel "ready"—after gathering information independently.

Are already motivated to revisit their mortgage due to external factors, such as changes in the economy, market conditions, or personal life events.

Behavioural Barriers Identified:

Despite their motivation, these clients hesitate to contact the bank early in the process due to key psychological barriers:

Fear of Appearing Incompetent

“I don’t want to look stupid by asking unrealistic or uninformed questions.”

High Need for Closure

Concern about feeling pressured into making a decision before they’re ready.

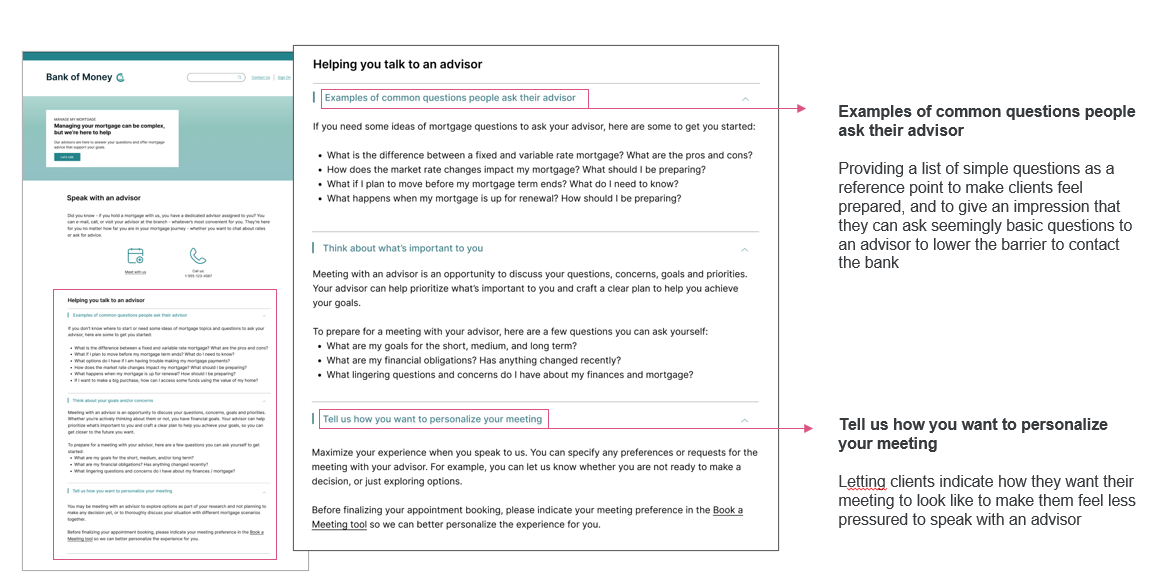

Behavioural Intervention (Nudging) #1

Behavioural principle used:

Channel factors: Adding additional materials to the existing Contact Us CTA that could make clients feel easy and less pressured to speak with an advisor

Hypothesis:

If we provide additional information that could help lower the psychological barrier to speak with an advisor, clients will be more likely to feel prepared and less pressured to speak with someone at the bank

Experiment design:

Recruited 132 participants who currently hold a mortgage in Canada

Divided them into two groups – one group with the nudge (treatment condition) and the other without (control)

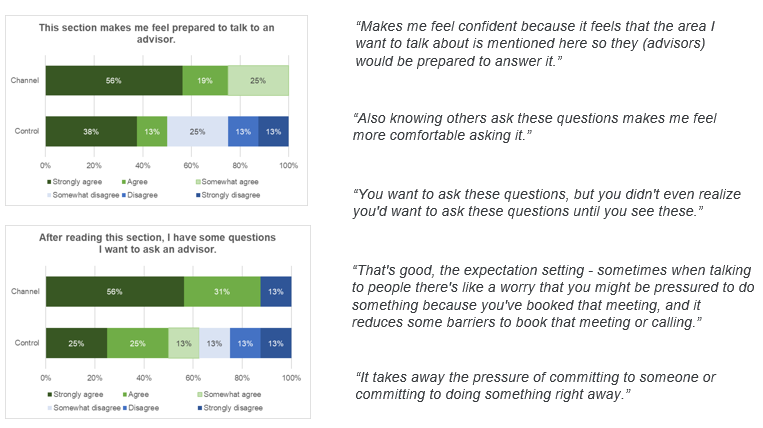

Both groups were asked to answer a series of questions (6-point likert scale) including:

This section makes me feel prepared to talk to an advisor.

I feel uncomfortable asking seemingly basic questions to an advisor.

If I speak with an advisor, I would feel pressured to make a decision during the meeting.

After reading this section, I have some questions I want to ask an advisor.

Results:

Compared to the Control group, participants in the Treatment group said...

They are less likely to feel pressured to make a decision during the meeting with an advisor.

They are more likely to find no problem asking seemingly basic questions to an advisor.

And also more likely to feel prepared and have enough information to talk to an advisor.

After reading the CTA section, they indicated that they are more likely to have questions they want to ask an advisor.

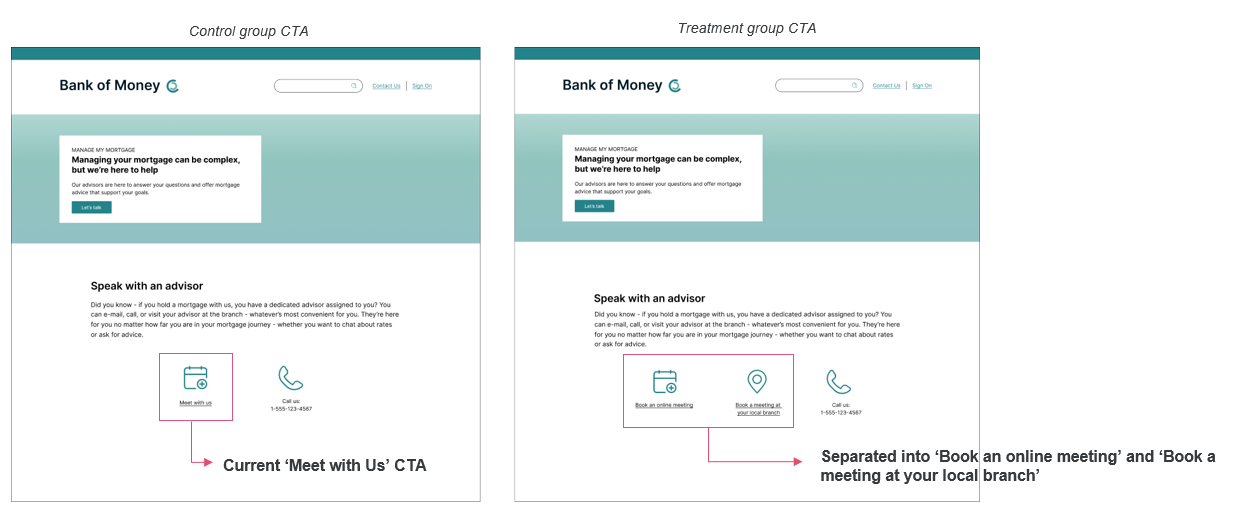

Behavioural Intervention (Nudging) #2

Behavioural principle used:

Decoy effect: Separating the current ‘Meet with Us’ CTA into two CTAs, ‘Book an online meeting’ and ‘Book a meeting at your local branch’ to make the online meeting option more attractive (assuming the in-branch option is the least appealing option for our clients)

Hypothesis:

If we separate the current ‘Meet with Us’ tool into two options – online and in-branch meetings and put them side by side, clients will be more likely to choose the online option (and increase the overall number of appointments booked than current state)

Experiment design:

Divided participants into two groups – one group with the treatment condition (three CTA options) and the other with the control condition (two CTA options)

Participants were asked out of the three (or two) contact options, which option they would like to choose to contact the bank

Results and learnings:

Participants in the Control group (two contact options – ‘Meet with Us’ or ‘Call Us’) preferred the call us option as they assumed ‘Meet with Us’ would be an in-branch meeting, while they just wanted to have a quick call to ask a couple of questions.

From participants in the Treatment group (three contact options - online meeting, in-branch meeting, and call), there was no significant difference between online vs in-branch meeting option unlike our hypothesis.

Although the intervention didn’t result in a significant impact in this experiment, we learned that it’s important to provide clients with context for each contact option to reduce confusion around what to expect and ultimately to encourage them to contact the bank by giving them confidence in their choices.

Impact

A net new ‘Manage My Mortgage’ page was implemented on the bank’s website. The behavioural interventions idea #1 was implemented within the Manage My Mortgage webpage.